to ₹1,605")

Blue Star Limited (NSE:BLUESTARCO) has just released its latest quarterly report and things are not looking great. The results seem to have been rather negative – revenue of ₹29 billion came in 3.2% below analyst estimates and statutory profit of ₹8.21 per share missed forecasts by 4.8%. Following the results announcement, the analysts have updated their earnings model and it would be good to know if they think there has been a big change in the company’s outlook or if it is business as usual. We thought readers would find it interesting to see the latest analysts’ (statutory) forecasts after earnings announcement for next year.

Check out our latest analysis for Blue Star

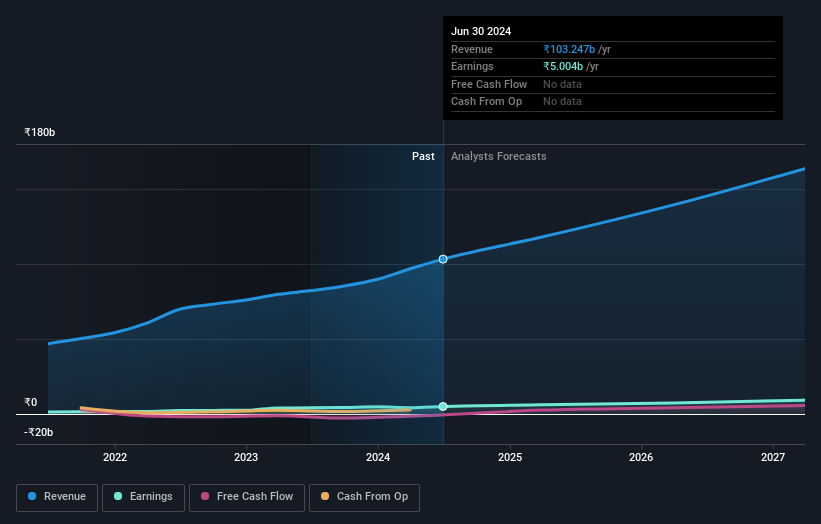

Taking into account the latest results, the latest consensus from 21 analysts for Blue Star is for revenues of ₹118.0 billion in 2025. If achieved, this will represent a notable 14% increase in sales over the past 12 months. Statutory earnings per share are expected to increase 19% to ₹29.04. Ahead of this report, analysts had modelled revenues of ₹118.1 billion and earnings per share (EPS) of ₹27.97 in 2025. So, the consensus seems to have become a bit more optimistic about Blue Star’s earnings potential following these results.

Analysts have been raising their price targets on the back of the earnings increase, with the consensus price target up 7.9% to ₹1,605. The consensus price target is just an average of individual analysts’ targets, so it might be useful to see how wide the range of underlying estimates is. There are some differing views on Blue Star, with the most optimistic analyst putting the value at ₹1,873 and the most pessimistic at ₹971 per share. These price targets show that analysts do have differing views on the company, but estimates don’t vary enough to suggest to us that some are betting on a huge success or an outright failure.

We can also look at these estimates in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether the forecasts are more or less optimistic when compared to other companies in the industry. From the latest estimates, we can conclude that the forecasts expect Blue Star’s historical trends to continuation, as the 19% annual revenue growth through the end of 2025 is roughly in line with the 17% annual growth over the past five years. Compare this to the broader industry, for which analyst estimates are expecting 15% annual revenue growth (on balance). So it’s pretty clear that Blue Star is expected to grow significantly faster than the industry itself.

The conclusion

The most important finding for us is the consensus upgrade to earnings per share, which suggests a significant improvement in sentiment around Blue Star’s earnings potential next year. Fortunately, they also confirmed their revenue numbers, suggesting they are in line with expectations. In addition, our data suggests that revenue is expected to grow faster than the wider industry. There was also a nice increase in the price target, as the analysts clearly feel that the company’s intrinsic value is improving.

However, the long-term development of the company’s earnings is much more important than the next year. We have forecasts for Blue Star up to 2027, which you can view here for free on our platform.

Please note, however, that Blue Star 2 warning signals in our investment analysis you should know about…

Valuation is complex, but we are here to simplify it.

Find out if Blue Star could be undervalued or overvalued with our detailed analysis, with Fair value estimates, potential risks, dividends, insider trading and the company’s financial condition.

Access to free analyses

Do you have feedback on this article? Are you concerned about the content? Contact us directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.