(NYSE:OBDC)")

Subscribe

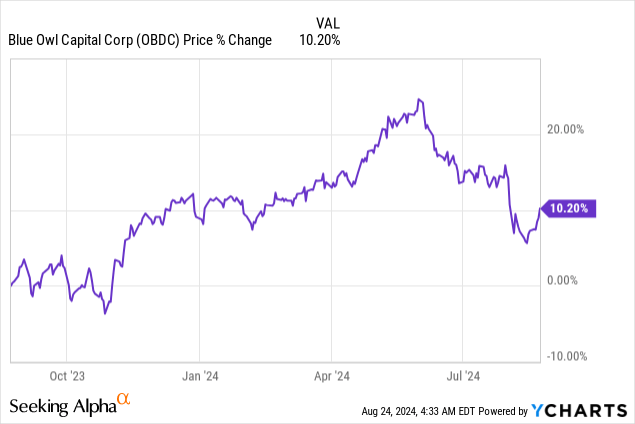

Shares of Blue Owl Capital (NYSE: OCD) have been steadily declining since I published my paper on BDC in May as the market feared an economic slowdown and lower interest rates. However, Blue Owl Capital maintained good asset quality and a robust distribution coverage profile in the second quarter, which continues to work in BDC’s favor. Blue Owl Capital is also merging with another business development company, which should provide benefits in terms of size, diversification and cost structure. What makes the shares particularly attractive from a return and risk profile perspective is that income investors can now buy Blue Owl Capital’s well-supported 12% yield below net asset value.

Previous review

I rated Blue Owl Capital shares a buy in May when they were trading at a 7% premium to net asset value, and I recommends Blue Owl Capital due to an improvement in the non-accumulation percentage: Why I’m buying Blue Owl Capital at a 1-year high. I also thought the dividend was fairly safe even if the Federal Reserve were to cut interest rates. Blue Owl Capital also announced a merger with Blue Owl Capital Corporation III (OBD), which should benefit the BDC’s portfolio and diversification metrics.

Senior lien strategy, asset quality and merger deal

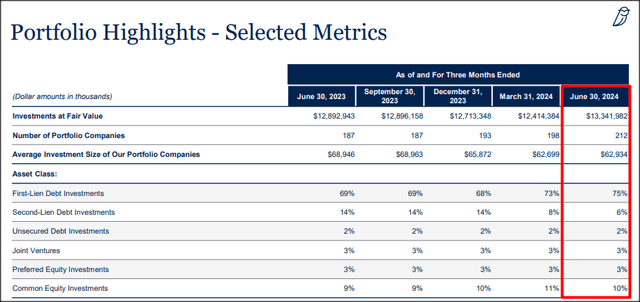

Blue Owl Capital pursues a senior secured credit strategy based on the BDC’s senior debt investments. The BDC invested primarily in senior debt in the second quarter, which represented 75% of all debt investments. An additional 6% of investments were second lien debt, resulting in a senior secured credit portion of ~82%.

Capital of the Blue Owl

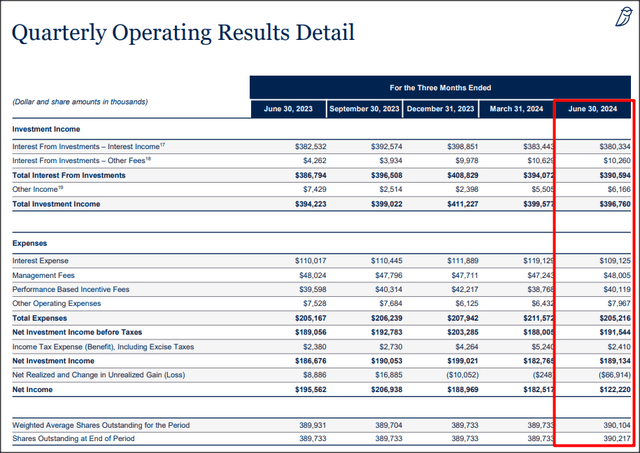

Blue Owl Capital generated net investment income of $189.1 million in the second quarter, up only about 1% year over year. Looking ahead, I don’t rule out a decline in net investment income, especially given the current inflation trend: Inflation was 2.9% in July, the fourth consecutive decline last month. This decline in the inflation rate prompted Jerome Powell last week to announce the first Federal Reserve interest rate cut next month. Since Blue Owl Capital is largely invested in floating rate debt (the floating rate share was 97% at the end of the June quarter), OBDC could see a decline in net investment income in the coming quarters.

Capital of the Blue Owl

Blue Owl Capital benefited from a sequential improvement in balance sheet quality and its non-accrual percentage decreased 0.4 percentage points quarter-on-quarter in the second quarter of 2024. At the end of the June quarter, Blue Owl Capital’s total non-accrual percentage was 1.4% and a total of six portfolio companies were designated as non-accrual companies, compared to five in the March quarter.

Let’s look at Blue Owl Capital’s merger agreement.

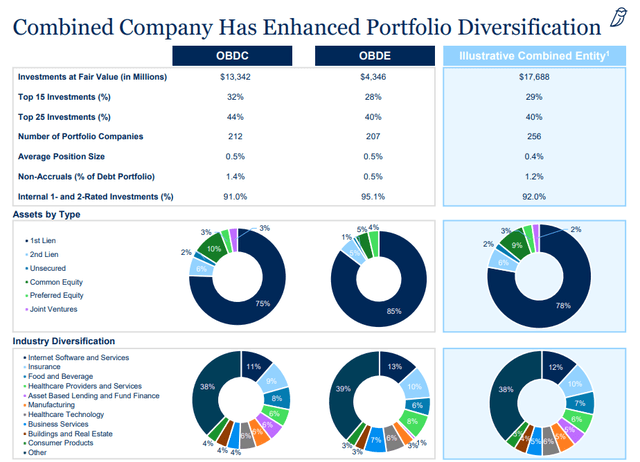

BDC announced in August that it would merge its business with Blue Owl Capital Corporation III to capture synergy and diversification benefits. The transaction is expected to close in the first quarter of fiscal 2025.

The merger of OBDC and OBDE will create the second largest BDC in the U.S. after Ares Capital (ARCC), with an estimated portfolio value of $17.7 billion. Because the portfolio has significant strategic overlap (including the same portfolio companies and debt securities), Blue Owl Capital’s first lien ratio is expected to increase to 78%, while its unaccrued lien ratio is expected to decrease to 1.2%.

Capital of the Blue Owl

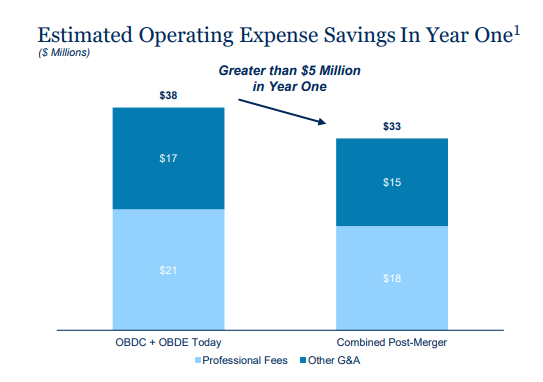

In addition, the portfolio combination of Blue Owl Capital would enable BDC to reduce its operating expenses, which could potentially have a positive impact on the company’s net investment income. According to the company’s merger summary, Blue Owl Capital expects to reduce its operating expenses by $5 million annually starting in year one.

Capital of the Blue Owl

The result of this merger will be a larger BDC with a more diversified portfolio that will be even more focused on high-quality first liens. An additional benefit is that OBDC will have better balance sheet quality (an off-balance sheet percentage of 1.2%) and the BDC shares may also provide better liquidity to investors.

Distribution coverage analysis

Blue Owl Capital’s Q1 2024 net investment income remained stable year-over-year: The BDC generated net investment income of $0.48 per share, representing a distribution coverage ratio of 1.12X… which is the same ratio as the previous quarter. Over the last four quarters, the BDC’s total distribution coverage ratio was 1.15, so I believe the BDC’s dividend has a high sustainability factor.

Capital of the Blue Owl

Review of Blue Owl Capital

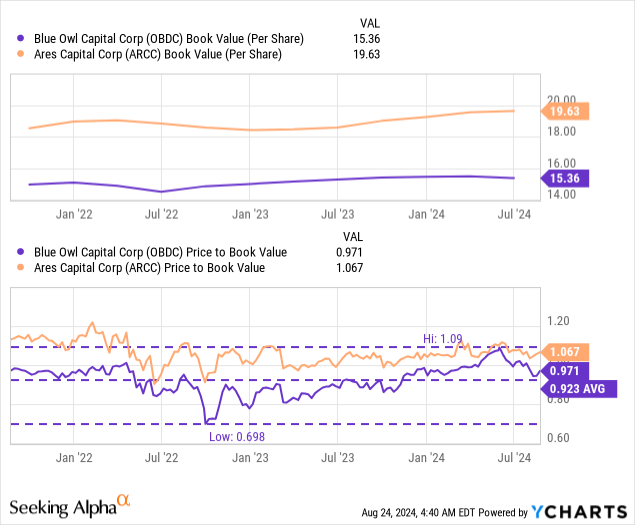

The main reason I like Blue Owl Capital is that BDC’s shares now trade at a (3%) discount to NAV… which was the main reason I double invested in BDC last week. Blue Owl Capital is valued at a price-to-NAV ratio of 0.97, making BDC comparatively more competitive: Ares Capital, the only BDC larger than Blue Owl Capital post-merger, trades at a 7% premium to NAV, and Blue Owl Capital has a merger catalyst that could cause a re-rating in the future.

When I last covered Blue Owl Capital, shares were trading at an XP/NAV ratio of 1.07, which is the same ratio Ares Capital has now. If Blue Owl Capital were to return to an XP/NAV ratio of 1.07, shares could have a fair value of ~$16.44 per share, representing about 10% upside potential.

Risks at Blue Owl Capital

Blue Owl Capital will see lower net investment income going forward when the Federal Reserve cuts its benchmark interest rate in September. Federal Reserve Chairman Jerome Powell said last week that the time for rate cuts has come and investors should take this seriously. Given that Blue Owl Capital has very good dividend coverage, I’m not worried about the 12% dividend yield.

Final thoughts

The merger of Blue Owl Capital with Blue Owl Capital Corporation III should be beneficial to shareholders. The new BDC is expected to become the second largest BDC in the market after Ares Capital, and the portfolio will be larger, more diversified, and have a lower proportion of off-balance sheet interests. In addition, cost synergies will increase Blue Owl Capital’s net investment income, so even if the Federal Reserve cuts the federal funds rate for the first time in September, the BDC should have no trouble covering its solid dividend going forward. Finally, I like the discount to net asset value, which makes the shares particularly attractive from a risk profile perspective.