")

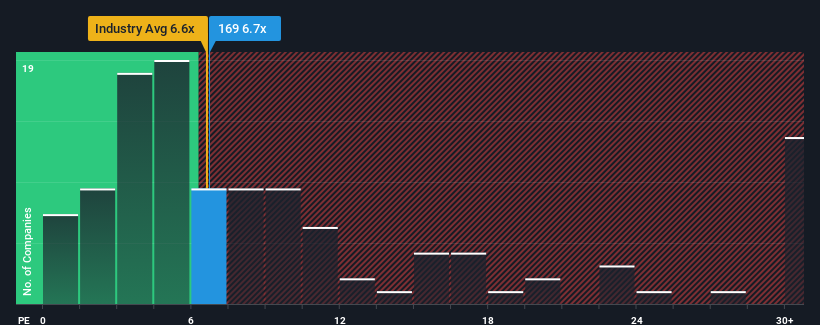

With nearly half of Hong Kong companies having a price-to-earnings (P/E) ratio of over 9x, you may consider Wanda Hotel Development Company Limited (HKG:169) with its P/E ratio of 6.7x is an attractive investment. However, the P/E ratio may be low for a reason and further research is needed to determine if it is justified.

For example, consider that Wanda Hotel Development’s financial performance has been poor recently as earnings have been declining. Many may expect the disappointing earnings performance to continue or accelerate, which has depressed the P/E ratio. If you like the company, you’d hope that doesn’t happen so you can potentially buy some shares while it’s out of demand.

Check out our latest analysis on Wanda Hotel Development

We don’t have analyst forecasts, but you can see how recent trends are positioning the company for the future by checking out our free Wanda Hotel Development earnings, revenue and cash flow report.

Does the growth match the low P/E ratio?

There is a fundamental assumption that a company must underperform the market for P/E ratios like Wanda Hotel Development’s to be considered reasonable.

If we look at last year’s earnings, the company’s earnings have fallen by a disheartening 15%. Despite this, earnings per share have increased by an admirable 432% compared to three years ago, regardless of the last 12 months. So, first of all, we can say that the company has generally done a very good job of growing its earnings during this time, even if there have been some hiccups along the way.

Comparing the recent medium-term earnings performance with the broader market’s one-year forecast of 18% growth shows that the company is significantly more attractive on an annual basis.

Given this information, we find it odd that Wanda Hotel Development is trading at a P/E ratio below market value. Apparently, some shareholders believe that recent performance has exceeded their limits and have accepted significantly lower selling prices.

The most important things to take away

Although the price-earnings ratio should not be the deciding factor in whether or not you buy a stock, it is still a useful indicator of earnings expectations.

We found that Wanda Hotel Development is currently trading at a significantly lower P/E than expected, as its recent growth over the past three years is higher than the broader market’s forecast. There could be some major, unnoticed threats to earnings that are preventing the P/E from carrying this positive trend. At a minimum, price risks appear to be very low if recent medium-term earnings trends continue, but investors seem to believe that future earnings could be very volatile.

Before you form an opinion, we found out 1 warning sign for Wanda Hotel Development that you should know.

It is important, Make sure you are looking for a great company and not just the first idea that comes to mind. So take a look at the free List of interesting companies with strong recent earnings growth (and low P/E ratios).

Valuation is complex, but we are here to simplify it.

Discover if Wanda Hotel Development could be under- or overvalued with our detailed analysis, with Fair value estimates, potential risks, dividends, insider trading and the company’s financial condition.

Access to free analyses

Do you have feedback on this article? Are you concerned about the content? Contact us directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.