NASHVILLE – The 16th annual Hotel Data Conference took place last week in Nashville and presented an extraordinary amount of data on the current state of the hotel industry.

In the first session, STR and Tourism Economics made slight adjustments to their US hotel forecast, but left RevPAR projects unchanged for the remainder of 2024 (+2%) and 2025 (+2.6%).

Hotel Investment Today also spoke with Jan Freitag, National Director of Hospitality Analytics at CoStar, about his thoughts on the various hotel segments, why public companies and REITs are drastically lowering their RevPAR forecasts for the rest of the year and the latest on leisure demand.

Here are some of the key insights we gained from various presentations at the Hotel Data Conference.

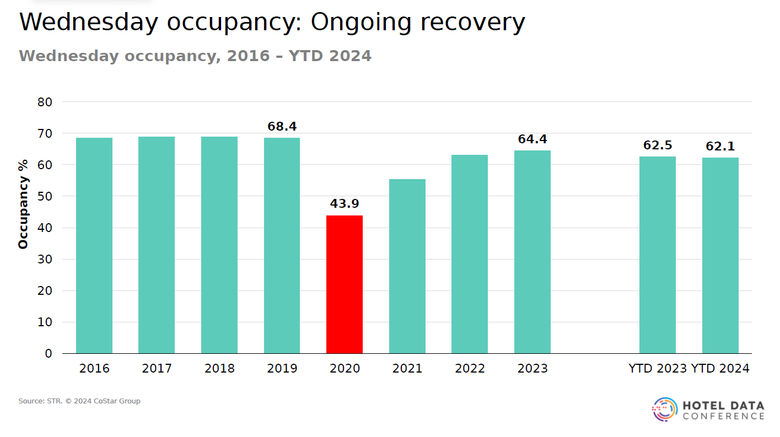

Wednesdays are the new Wednesdays

By Jan Freitag

Freitag looked at how midweek demand, namely Wednesdays, has fared post-COVID for U.S. hotels. He said Wednesdays are a key indicator of midweek demand because from 2010 to 2019, Wednesday occupancy for hotels was higher (66%) on all days except Friday (67.3%) and Saturday (69.4%). He mentioned a dramatic $32 ADR decline in 2020 for the industry, including an apocalyptic 9.7% average occupancy for Wednesdays in April 2020.

Those numbers have risen dramatically since then, with Wednesday ADRs reaching $152 in 2023 and $155 in 2024. Wednesday ADR growth rose 6% from 2016 to 2019, and after the 2020 plunge, inflation has helped boost Wednesday ADR growth by 6% from 2022 to 2023.

However, Freitag said that by segmenting demand for short-term and group travel, it is clear that hotels are still missing millions of travelers. Short-term demand is still down 3% from 2019 to 2023, and group travel demand is down 8% from 2019 to 2023. So who is to blame? An easy culprit would be an incomplete increase in office footfall since 2019. He said that while office footfall is increasing, it is still nearly half of what it was before the COVID outbreak.

“It’s very clear that weekday demand is recovering, and recovering quite nicely, except that we’re not back to pre-COVID levels in terms of total transient rooms sold,” Freitag said in an interview with Hotel Investment Today. “Why is that? I argue that it’s partly because we don’t need as much travel because we’re not all in the office all the time… I argue that the transient part is a little limited, but on the group side… everything seems to point to groups being the most important thing. That’s what people want.”

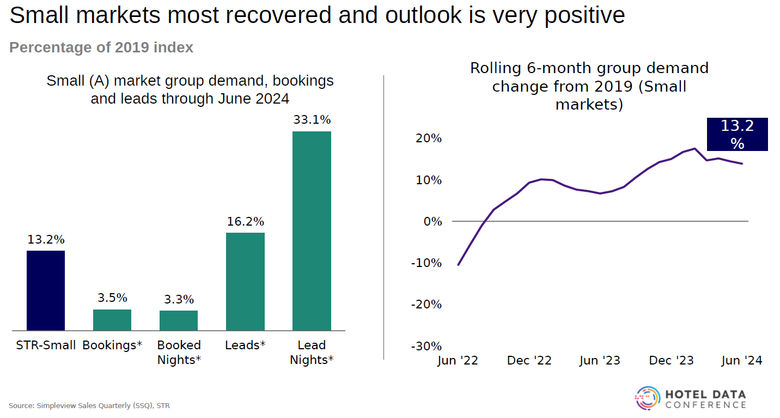

Group trends and booking pace

By Chris Klauda, Senior Director at STR and Vail Ross, Managing Director of 2Synergize.

The presentation said that group demand has almost caught up with overall demand when comparing pre-COVID numbers to current levels, but there remains a larger ADR gap between transient and group travel in 2024 than at the onset of COVID.

According to Simpleview’s quarterly sales data, aggregate lead volume has recovered from 2019 and will increase starting in 2023. Aggregate lead room nights started the year strong, nearly 31% higher than 2019 and nearly 12% higher than a year ago.

Simpleview has divided the markets into four categories: large convention centers with 46,000 square meters of gross area, mid-sized convention centers with 9,000 to 46,000 square meters of gross area, small convention centers with less than 9,000 square meters of gross area, and small markets without major convention facilities.

The data shows that the smaller markets have recovered the fastest from 2019 and are also very positive about the future, while the larger markets still have the longest way to go in their recovery.

The presentation concluded that group demand continues to grow and weekdays have fully recovered to 2019 levels. Lead volumes are up, but bookings are down compared to 2019. Nevertheless, there is general optimism for the meetings and events business across the industry, with smaller markets set to recover the fastest.

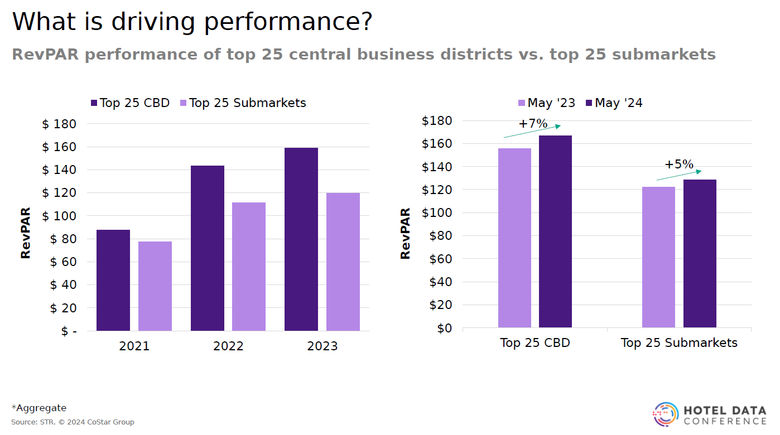

Renaissance of the Top 25: Are CBDs driving growth?

By Colin Sherman, Director of Hospitality Analytics, US South for CoStar

The presentation found that RevPAR grew faster in the top 25 markets than in all other markets. This trend was somewhat less pronounced during the COVID pandemic, but is now back to pre-2019 levels. Over the past 12 months, with the exception of March, RevPAR grew faster in the top 25 markets than in other markets.

The central business districts (CBDs) of the top 25 markets have 30% of the supply but 37% of the revenue compared to their corresponding submarkets. In May, RevPAR in the top 25 CBDs increased 7% year-over-year, while it increased 5% in the top 25 submarkets. Occupancy increased 3% year-over-year in both categories, and ADR increased 2%.

However, the presentation stated that the submarkets are doing their part and contributing to the performance of their markets, particularly in transient occupancy, where the submarkets are ahead of their CBD counterparts.

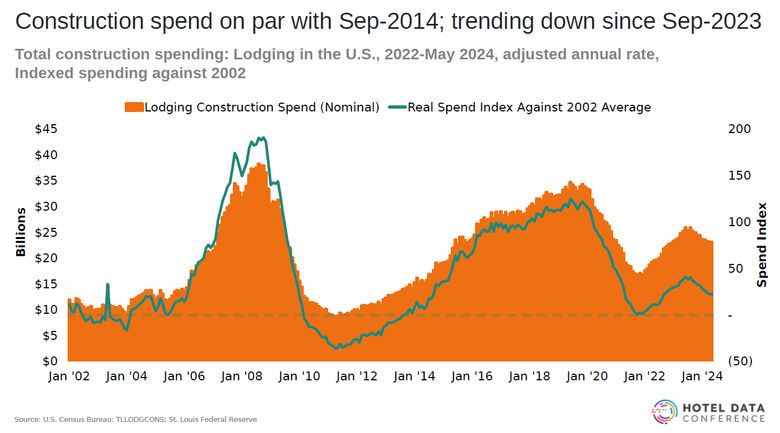

What’s in the pipeline?

By M. Brian Riley, senior research analyst at STR

The presentation said that construction is resuming, but it is still slow and many development plans are still in the pipeline. There is still a “wait and see” phase in terms of hotel construction, as construction spending is at its lowest level in almost 10 years. The biggest obstacles are affordable financing and the ever-increasing cost of goods, as many are waiting for inflation and interest rates to drop.

Due to these trends, the greatest surge in activity is currently being seen in the conversion of hotels rather than new construction.

New room supply is not growing strongly (+0.6% through June), but pipeline activity totals over 758,000 rooms in the US, up 15.6% from 2019 and 19.7% from 2023. The majority of this growth is accounted for by the 334,000 rooms in the planning phase, up 38.7% year-on-year.

While the number of 158,000 rooms currently under construction increased 5.5% year over year (with New York City, Nashville, Detroit, Miami and Phoenix leading the pack), the presentation said construction spending was at September 2014 levels but trending downward compared to September of the previous year.

The presentation also said that more hotels have switched from one company to another in recent years (but well below their early 2010s peaks), while the number of switches from branded hotels to independents is lower than it was 10-15 years ago. It also said that over the past two years, hotels have been just as likely to move up a chain tier as down, and that lower-tier chains still lead the way in conversion activity.