Subscribe

Key findings

- The fund lagged behind the S&P 500 Index (SP500, SPX).

- The Fund’s holdings in information technology (“IT”) and industrials contributed most to relative returns.

- Low market participation impaired relative performance

- Smaller stocks lagged behind mega-cap stocks. This was a headwind for the fund because its equal-weighting method naturally leads to underweights in the largest index stocks and overweights in the smaller index stocks.

- Possible opportunities for an equilibrium strategy

- The almost identical position size reduces concentration risk compared to the S&P 500 Index, where the largest companies represent the largest exposures. In addition, the fund is valued lower than the capitalization-weighted index.

Manager perspective and outlook

The similarities between the first and second quarters may have created a sense of déjà vu among investors. In the second quarter, the S&P 500 Index, with a return of 4.28%, outperformed the S&P MidCap 400 Index (MID:IND, -3.45%) and the S&P SmallCap 600 Index (-3.11%), while the S&P 500 Growth Index outperformed the S&P 500 Value Index (9.59% vs. -2.10%). IT and communications services were two of the best-performing sectors, and a small group of mega-cap growth companies had a disproportionate impact on the index results. These trends are all reminiscent of the first quarter.

The split returns were, in our view, a symptom of crosscurrents in economic data. While some second-quarter data pointed to a strong economy, others signaled to us potential weakness. Positive indicators — easing inflation, a robust labor market and prudent balance sheet management — helped accelerate earnings. Negative surprises included the ISM manufacturing purchasing managers’ index, which declined for its third straight month in June, and the University of Michigan consumer sentiment survey, which fell to a seven-month low in June. The fund’s equal-weight methodology means the fund historically offers greater exposure to smaller stocks and lower-valued stocks. These exposures have been a headwind in an environment where large caps have outperformed small and mid caps and growth has outperformed value.

Portfolio positioning

Concentration appears to continue to be a problem in the U.S. stock market for large companies, as a handful of small companies make up an ever-larger portion of the market. After a rapid growth rally in the second quarter, concentration levels during the pandemic exceeded the previous cycle peak. The total weight of the top 10 companies in the S&P 500 Index was just over 37% at the end of the quarter. Although the index contains about 500 stocks, over a third of its value is concentrated in just 10 companies—the highest concentration since the late 1970s. For comparison, the average weight of the top 10 holdings in the S&P 500 Index over the past 35 years has been about 21%, and before the most recent post-pandemic cycle, the peak was 27% (reached in June 2000, just before the dot-com bubble burst). Historical concentration extends to sectors as well. The technology share was 32.4% at the end of the quarter, above the previous cycle high of 29.2% in 1999.

Although the current period of extreme concentration is detrimental to the Fund’s relative performance, a return to less extreme levels of concentration could have a positive impact on the Fund’s relative return.

Recently, investors have seemed to attribute a higher growth premium to the S&P 500 Index than to the S&P 500 Equal Weight Index, which has contributed to the former’s outperformance over the latter. For example, S&P 500 Index earnings declined 0.9% year-over-year in 2023, while S&P 500 Equal Weight Index earnings actually rose 2.9%. Nevertheless, the S&P 500 Index still outperformed the S&P 500 Equal Weight Index by 12.4% in 2023, as the S&P 500 Index’s price-to-earnings (P/E) ratio rose 25.2%, compared to a 9.6% increase in the S&P 500’s P/E ratio.

S&P 500 Equal Weight Index. With the tailwind of more favorable year-over-year earnings comparisons through 2024, analysts are forecasting earnings growth of 10.6% for the S&P 500 Index in 2024 versus 6.2% for the S&P 500 Equal Weight Index (Source: Bloomberg). Once again, the S&P 500 Index’s outperformance of the Equal Weight Index year-to-date has been supported by multiple expansion. The S&P 500 Index’s P/E ratio rose 11.3% through June 30 versus 2.8% for the Equal Weight Index. At quarter-end, the S&P 500 Index’s P/E ratio of 25.6x represented a 21.5% premium to its 10-year average of 21.5x. The S&P 500 Equal Weight Index’s P/E ratio of 19.6 represented a discount of 2.9% from its ten-year average of 20.2.

Largest issuers (% of total net assets)

|

Funds |

index |

|

|

FedEx Corp (FDX) |

0.24 |

0.24 |

|

Carnival Corp (CCL) |

0.24 |

0.24 |

|

Norwegian Cruise Line Holdings Ltd (NCLH) |

0.22 |

0.23 |

|

Synchrony Financial (SYF) |

0.22 |

0.22 |

|

Baker Hughes Co (BKR) |

0.22 |

0.22 |

|

MGM Resorts International (MGM) |

0.22 |

0.22 |

|

Tesla Inc. (TSLA) |

0.22 |

0.22 |

|

Salesforce Inc. (CRM) |

0.22 |

0.22 |

|

Intuit Inc (INTU) |

0.22 |

0.22 |

|

Caesars Entertainment Inc (CZR) |

0.22 |

0.22 |

|

As of June 30, 2024. Stocks are subject to change and do not constitute buy/sell recommendations. |

||

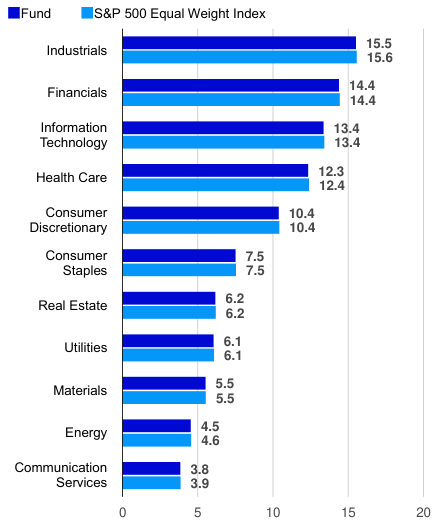

Breakdown by sectors (% of total net assets)

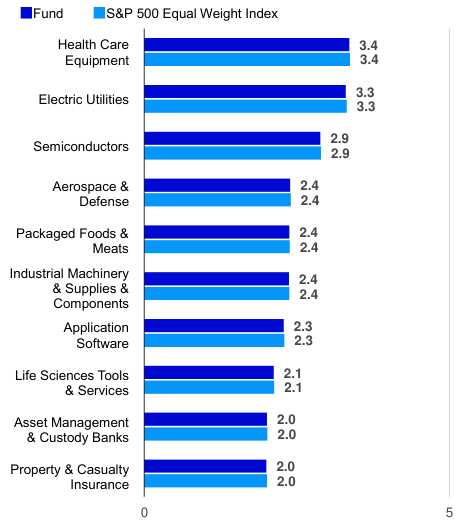

Top industries (% of total net assets)

Performance highlights

The Invesco Equally-Weighted S&P 500 Fund returned -2.77% for the quarter, while the S&P 500 Index returned 4.28%. Over the course of the quarter, market participation declined and breadth was thin, with smaller stocks showing less participation.

The fund’s underperformance versus the S&P 500 Index in the second quarter was largely due to the equal-weighted allocation methodology, which creates a natural bias toward smaller stocks within the index.

Top performers

First Solar (flsr): The semiconductor company is primarily benefiting from the increasing focus on electrification and rising electricity demand due to the widespread adoption and implementation of artificial intelligence (AI). Analysts highlighted the direct impact of AI on First Solar’s business results, forecasting a rise in earnings per share as major technology companies appear to be looking for sustainable energy sources to power AI.

NVIDIA (NVDA): The semiconductor and equipment company remained the darling of the long-term growth trend in the AI sector. With its latest quarterly report, Nvidia once again exceeded analysts’ expectations. Management’s sales forecast also exceeded analysts’ expectations.

Factors that reduce performance

Walgreens Boots Alliance (WBA): This consumer goods company’s stock price fell after management lowered its earnings forecast for the fiscal year, citing a deteriorating retail environment. Walgreen’s management also announced an increase in planned store closures, which further pushed down the stock price.

Builders First Source (BLDR): The home products company’s share price plunged as management cited a weakening housing market and higher mortgage rates as headwinds. Management mentioned expectations of another sharp decline in the multifamily sector, with a consistent year-over-year decline through the end of 2024.

Largest contributors (%)

|

Issuer |

Return |

Contribution to return |

|

First Solar, Inc. |

33.57 |

0.08 |

|

NVIDIA Corporation |

36.74 |

0.08 |

|

Teradyne, Inc. (TER) |

31.54 |

0.07 |

|

NetApp, Inc. (NTAP) |

23.29 |

0.05 |

|

Apple Inc. (AAPL) |

22.99 |

0.05 |

Biggest critics (%)

|

Issuer |

Return |

Contribution to return |

|

Walgreens Boots Alliance, Inc. |

-43.45 |

-0.10 |

|

Contractor FirstSource, Inc. |

-33.63 |

-0.07 |

|

Estee Lauder Companies Inc. (EL) |

-30.61 |

-0.07 |

|

Paycom Software, Inc. (PAYC) |

-27.97 |

-0.06 |

|

Intel Corporation (INTC) |

-29.60 |

-0.06 |

Standardized performance (%) as of June 30, 2024

|

quarter |

Annual course |

1 year |

3 years |

5 years |

10 years |

Since its founding |

||

|

Class A shares (MUTF:VADAX) Start: 28.07.97 |

Net asset value |

-2.77 |

4.81 |

11.23 |

4.30 |

10.37 |

9.46 |

9.06 |

|

Max. load 5.5% |

-8.11 |

-0.96 |

5.11 |

2.35 |

9.13 |

8.84 |

8.83 |

|

|

Class R6 shares (MUTF:VADFX) Start: 24.09.12 |

Net asset value |

-2.68 |

4.99 |

11.62 |

4.66 |

10.77 |

9.85 |

12.07 |

|

Class Y Shares (MUTF:VADDX) Start: 28.07.97 |

Net asset value |

-2.70 |

4.94 |

11.52 |

4.56 |

10.65 |

9.73 |

9.32 |

|

S&P 500 Equilibrium Index |

-2.63 |

5.08 |

11.79 |

4.84 |

10.94 |

10.04 |

– |

|

|

Total return ranking compared to Morningstar Large Blend category (Class A shares at net asset value) |

– |

– |

94% (1336 of 1417) |

90% (1207 of 1304) |

88% (1061 of 1197) |

88% (788 of 893) |

– |

|

Expense ratios according to the current sales prospectus: Class A: Net: 0.52%, Total: 0.52%; Class R6: Net: 0.18%, Total: 0.18%; Class Y: Net: 0.27%, Total: 0.27%. The performance shown is past performance and does not guarantee comparable future results; actual performance may be lower or higher. Visit Country Splash for performance to the last month end. Performance figures reflect reinvested distributions and changes in net asset value (NAV). Investment return and capital value may vary so you A gain or loss may be incurred when shares are sold. Returns of less than one year are cumulative, all others are annualized. Index source: RIMES Technologies Corp. If fees had not been waived and/or expenses reimbursed in the past, returns would have been lower. Performance shown in net asset value does not include the applicable sales charge, which would have reduced performance. Class Y and R6 shares do not have an initial charge and therefore performance is at net asset value. Class Y shares are only available to certain investors. Class R6 shares are closed to most investors. Please refer to the prospectus for further details. For further information, including the prospectus and fact sheet, please visit Invesco.com/VADAX. Not a deposit Not insured by the FDIC Not guaranteed by the bank May lose value Not insured by any federal agency |

Original post

Editor’s note: The summary points for this article were selected by the editors of Seeking Alpha.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these securities.