phakphum patjangkata/iStock via Getty Images

Key findings

- The fund recorded a decline during the quarter.

- REITs underperformed the broader equity markets, with REIT sectors that are historically more vulnerable to high interest rates – timber, industrials and infrastructure – lagging.

- The fund aims to achieve a balance between selected structural growth opportunities and historically economically sensitive REITs at reasonable valuations.

- The fund is geared towards a positive but below-average economic growth environment, which would favor positioning in REITs with visible potential growth opportunities.

- The prospect of falling interest rates and moderate growth could mean good investments Opportunities in real estate.

- We have observed that listed real estate has delivered strong returns relative to broader equities following the last rate hike as part of a Federal Reserve tightening cycle.

Manager perspective and outlook

General stocks posted a positive return while REITs posted a negative return for the quarter. Real estate transaction activity has been constrained by limited availability and increased capital costs over the past two years, creating a large gap between buyers’ and sellers’ price expectations. Full normalization of the real estate transaction market may take some time as interest rates and capital costs have remained high for many property types.

REIT unsecured debt issuance has increased in recent months as bond market conditions appear to have improved. REITs with access to unsecured credit have an advantage over private real estate markets, which have historically relied heavily on secured financing. Publicly traded real estate companies, which have favorable capital costs compared to private real estate investors and also have strong operating platforms, are most likely to find attractive investment opportunities.

Portfolio positioning

With a further acceleration in economic growth unlikely and interest rate cuts expected in 2024, the Fund has added to select low-valuation opportunities. We have also increased the Fund’s position in single-family rental properties, which we believe should continue to benefit from a structural housing shortage exacerbated by persistently high interest rates.

Recent additions to the fund include holdings in historically more interest rate sensitive sectors such as triple net, infrastructure and healthcare physician office REITs. During the quarter, we shifted our exposure to data centers to take advantage of relative valuation opportunities.

The fund’s current overweights include life sciences, healthcare and single-family rental REITs. The fund is underweight retail, multifamily and industrial REITs. We believe the retail and multifamily sectors have unattractive growth and valuation characteristics relative to other property types, while the industrial sector has weakening fundamentals at a still-high valuation.

Looking ahead, changes in macroeconomic data, the fundamental outlook, interest rates and the monetary policy outlook can impact our relative value views and resulting fund positioning.

Largest issuers (% of total net assets)

|

Funds |

index |

|

|

American Tower Corp (AMT) |

9.84 |

7.26 |

|

Welltower Inc (WELL) |

8.27 |

4.93 |

|

Equinix Inc (EQIX) |

7.71 |

5.73 |

|

Extra Space Storage Inc (EXR) |

4.90 |

2.60 |

|

Housing Equity (EQR) |

4.83 |

2.09 |

|

Camden Property Trust (CPT) |

4.72 |

0.90 |

|

Healthpeak Properties Inc (DOC) |

4.11 |

1.11 |

|

Invitation Homes Inc (INVH) |

4.03 |

1.76 |

|

Alexandria Real Estate Equities Inc (ARE) |

4.00 |

1.62 |

|

Rexford Industrial Realty Inc (REXR) |

3.95 |

0.77 |

|

As of June 30, 2024. Stocks are subject to change and do not constitute buy/sell recommendations. |

||

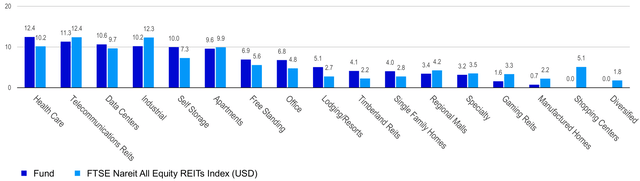

Breakdown by sector (% of total net assets)

Performance highlights

Invesco Global Equity Fund (MUTF:IARCX) posted a negative return and underperformed its benchmark.

Top performers

During the quarter, the Fund benefited from an overweight in the healthcare sector, which outperformed due to positive results from the senior living space and selected value opportunities. The positive impact of the Fund’s overweight in the healthcare sector offset negative stock selection in the sector. Stock selection in the infrastructure and freestanding real estate sectors also contributed to relative performance.

The fund was overweight in the multifamily sector for most of the quarter, which contributed positively to relative returns as the sector outperformed, boosted by privatization and a labor market that remained stable despite low expectations.

Factors that reduce performance

Both stock selection and sector allocation detracted from relative performance during the quarter. The overweight to timber REITs was the largest detractor from relative returns. Timber stocks underperformed as persistently high interest rates weighed on residential construction activity. An underweight to Eisenberg (IRM) was also negative for relative performance.

Largest contributors (%)

|

Issuer |

Return |

Contribution to return |

|

Welltower Inc. |

12.26 |

1.00 |

|

Camden Real Estate Trust |

11.77 |

0.58 |

|

Equity housing |

9.72 |

0.47 |

|

Extra Space Storage Inc. |

6.80 |

0.32 |

|

Agree Realty Corporation (ADC) |

9.72 |

0.25 |

Biggest critics (%)

|

Issuer |

Return |

Contribution to return |

|

Weyerhaeuser Company (WY) |

-20.42 |

-0.87 |

|

Host Hotels & Resorts, Inc. (HST) |

-12.11 |

-0.64 |

|

Prologis, Inc. (PLD) |

-13.01 |

-0.54 |

|

Rexford Industrial Realty, Inc. |

-10.52 |

-0.50 |

|

Terreno Realty Corporation (TRNO) |

-10.23 |

-0.45 |

Standardized performance (%) as of June 30, 2024

|

quarter |

Annual course |

1 year |

3 years |

5 years |

10 years |

Since its founding |

||

|

Issue of Class C shares: 01.05.95 |

Net asset value |

-1.73 |

-3.69 |

2.28 |

-3.57 |

0.51 |

3.79 |

8.74 |

|

Issue of Class A shares: 31.12.96 |

Net asset value |

-1.48 |

-3.36 |

3.06 |

-2.83 |

1.27 |

4.43 |

7.90 |

|

Max. load 5.5% |

-6.90 |

-8.66 |

-2.58 |

-4.64 |

0.13 |

3.84 |

7.68 |

|

|

Issue of share class R6: 24.09.12 |

Net asset value |

-1.43 |

-3.14 |

3.49 |

-2.43 |

1.73 |

4.90 |

5.80 |

|

Launch of Class Y shares: 03.10.2008 |

Net asset value |

-1.48 |

-3.31 |

3.25 |

-2.62 |

1.51 |

4.68 |

6.62 |

|

FTSE Nareit All Equity REITs Index (‘USD’) |

-0.90 |

-2.19 |

5.78 |

-1.63 |

3.40 |

6.11 |

– |

|

|

Total return ranking compared to the Morningstar Real Estate category (Class C shares at net asset value) |

– |

– |

88% (218 of 235) |

88% (200 of 223) |

90% (188 of 204) |

86% (131 of 149) |

– |

|

|

Expense ratios according to the current sales prospectus: Class C: Net: 2.00%, Total: 2.00%; Class A: Net: 1.25%, Total: 1.25%; Class R6: Net: 0.80%, Total: 0.80%; Class Y: Net: 1.00%, Total: 1.00%. Performance shown is past performance and is not a guarantee of similar future results. Current performance may be higher or lower. Performance to the most recent month end can be found on invesco.com. Performance figures reflect reinvested distributions and changes in net asset value (NAV). Investment return and capital value may fluctuate so you may have a gain or a loss when you sell shares. Returns of less than one year are cumulative; all others are annualized. Index source: RIMES Technologies Corp. If fees had not been waived and/or expenses reimbursed in the past, returns would have been lower. Performance shown at NAV does not include the applicable sales charge, which would have reduced performance. |

|

Redemptions of Class C shares will not be subject to a CDSC after one year from the date of purchase. Performance shown at net asset value does not include any initial charge which would have reduced performance. Class Y and R6 shares have no initial charge and therefore performance is equal to net asset value. Class Y shares are only available to certain investors. Class R6 shares are closed to most investors. Please refer to the prospectus for further details. |