")

Sharpness86

Note:

I have covered Plug Power Inc. or “Plug Power” (PLUG), so investors should consider this an update to my previous articles on the company.

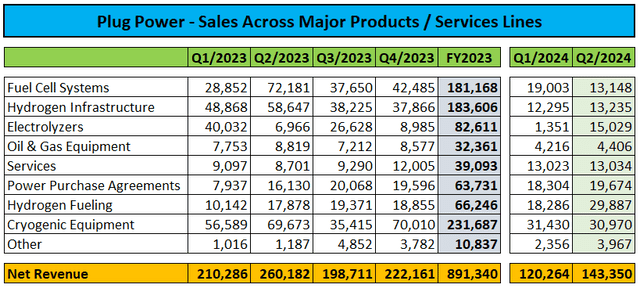

Two weeks ago, Plug Power again reported disappointing quarterly results. Revenue missing Consensus expectations once again by far.

Applications for approval

Revenues fell 45% year-over-year, with the company’s core business of fuel cell systems and hydrogen infrastructure taking a particularly heavy hit after Plug Power increased prices on its product and service offerings and virtually stopped providing lease financing to customers.

Although the company’s electrolyzer segment increased quarter-on-quarter and year-on-year, it continued to struggle as Plug Power deployed over $70 million worth of electrolyzers during the quarter but was unable to capitalize on “Final commissioning and testing requirements“.

The segment has The impact on the company’s financial results has been a major drag for several years now. Demand for electrolyzers has been well below management’s initial expectations, leading to delays or even cancellations of backlogged projects. In addition, management had initial contracts signed well below cost, resulting in severely negative product margins.

However, Plug Power’s hydrogen tanking segment was a big positive surprise, with revenues boosted by price increases and, to a lesser extent, the recognition of assumed production tax credits in the company’s financial results. As Plug Power’s first green hydrogen plant in Georgia ramps up production, the company’s overall hydrogen cost base reduced. Tanking revenues increased more than 60% quarter-over-quarter, leading to a corresponding increase in gross margin.

Applications for approval

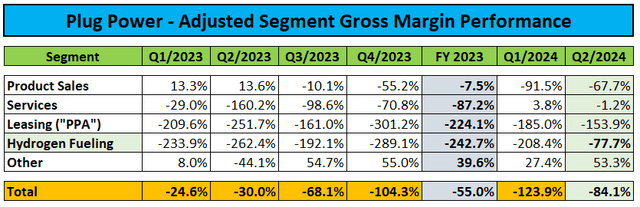

Adjusted for the accounting impact of the warrants issued to the main customers Amazon (AMZN) and Walmart (WMT), the segment margin improved from -208.4% in the first quarter to -77.7% in the second quarter.

Applications for approval

Recent price increases for the Company’s product and service offerings combined with recent restructuring actions resulted in adjusted consolidated gross margin improving from -123.9% to -84.1% quarter-over-quarter.

In the conference call, management commented on its expectations for further progress in the second half of the year:

Since January 1, we have reduced our global workforce by over 15% due to the first quarter restructuring and ongoing attrition where we did not fill positions. We have adjusted pricing across many equipment, fuels and service platforms, which is reflected in our second quarter results, particularly fuel and service. This pricing impact will be even greater throughout the remainder of the year as we receive full periods under these structures and implement additional pricing actions.

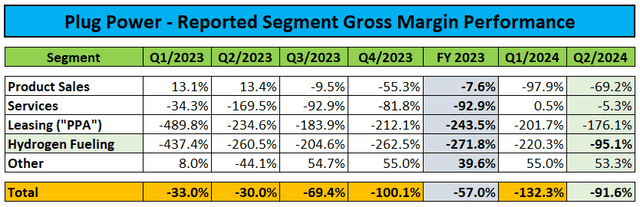

However, increased cash consumption remains a cause for concern.

Applications for approval

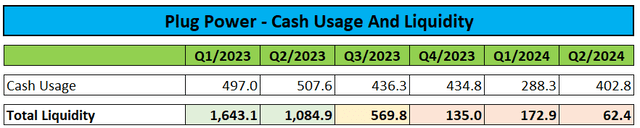

During the quarter, the company burned through $402.7 million in cash. Combined with first-quarter cash burn of $288.3 million, Plug Power has already exceeded management’s implied full-year cash burn target of $500 million by nearly 40%.

To replenish its dwindling cash reserves, the company continued to aggressively sell new shares on the open market. During the second quarter, the company raised an additional $266.8 million under its ATM agreement with a division of B. Riley Financial (RILY), ending the quarter with unrestricted cash and cash equivalents of just $62.4 million.

After the quarter ended, the company sold additional shares in the open market, raising estimated net proceeds of $29.8 million. In addition, Plug Power raised net proceeds of $191 million from an underwritten public offering last month.

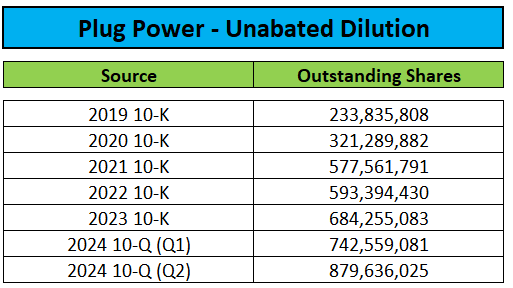

As a result, there has been a massive dilution of ordinary shareholders’ shares since the beginning of the year.

Applications for approval

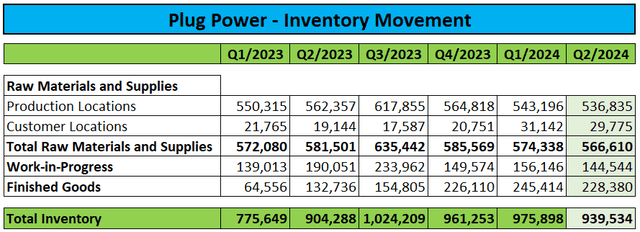

In the conference call, management expressed its expectation that cash burn will decline significantly in the second half of the year, primarily due to the expected release of up to $250 million in working capital due to lower inventory levels.

Applications for approval

However, given the inventory movements of the last few quarters, I do not expect the company to come anywhere close to achieving its stated goal.

Not surprisingly, management remained optimistic about the company’s ability to take advantage of the Department of Energy’s $1.66 billion conditional loan guarantee:

We have made tremendous progress. We meet with them regularly and will meet again in two weeks to continue their final due diligence and move the process forward. We are fully clear on the actions and processes to successfully close this facility. And just as importantly, the Department of Energy has clearly expressed its interest and support for a quick closure. This facility is expected to provide immediate liquidity and allow us to accelerate the build-out of the Texas green hydrogen facility.

For my part, I do not expect the loan to expire anytime soon, as the Department of Energy will likely impose tough conditions to protect taxpayers’ money – especially given management’s abysmal track record.

Looking ahead, management forecasts annual revenue in a range of $825 million to $925 million. To reach the lower end of the forecast, revenue in the second half of the year would have to more than double compared to the first half of 2024.

Given the ongoing headwinds in its business performance and the company’s decades-long history of overpromising and underdelivering, I would expect Plug Power to miss the lower end of its range by a wide margin, much like it has in previous years.

Conclusion

As usual, Plug Power’s second-quarter 2024 results fell far short of consensus expectations. Worse, the company continues to burn cash at a rapid pace, resulting in ongoing dilution for common shareholders.

However, it wasn’t all bad, as the company made progress on margins. Particularly encouraging was the significant improvement in Plug Power’s hydrogen tank segment.

Unfortunately, management has not learned from its mistakes and has again made its full-year sales forecast too ambitious. This means that the company’s decade-long pattern of overpromising and underdelivering is likely to continue unabated.

Although I expect Plug Power to miss its full-year forecasts by a long shot, I rate the company’s stock at “Sell” To “Hold” based on the encouraging margin trends of the quarter.