")

IL21/iStock via Getty Images

Investment thesis

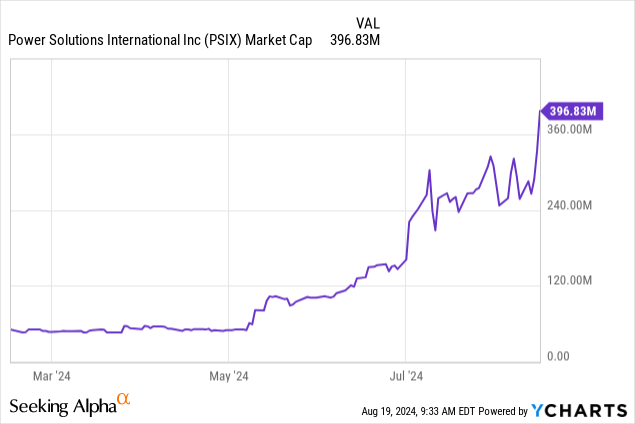

Many investors were surprised by the meteoric rise of Power Solutions International (OTCPK:PSIX). In just three months, the Pink Sheets stock maker increased its market capitalization from $60 million to $400 million. This monumental change gives a the impression of a dramatic improvement in the company’s fundamentals. However, this is not the case, as reflected in the declining sales. On the other hand, PSIX’s margin improvement is a reminder that this once NASDAQ-listed company should not be trading on pink sheets either.

A fallen angel

The company fell from grace in 2016 – just five years after its IPO – when it was accused of artificially inflating 2015 revenue by $25 million, or 11.5%, according to a September 2020 cease-and-desist order. Sure, the scandal was painful, but the extent of the accounting error was disproportionate to the reaction that followed. PSIX was paralyzed after the allegations came to light. The CFO resigned, the COO ratted out his colleagues, financial reports were stopped, conference calls on quarterly results were stopped and communication with the NASDAQ (NDAQ), after which the company was soon delisted from the stock exchange. It was a rather bizarre situation that forced PSIX to capitulate to the Pink Sheets OTC market. And all this for only $25 million, allegedly a revenue discount scheme over 5 quarters, a figure that represents only 11.5% of the total annual revenue.

In 2017, Weichai Power (OTCPK:WEICF), China’s largest engine maker, acquired a majority stake in PSIX. At the time, PSIX had already been delisted from NASDAQ and hadn’t released its financials in years, but WEICF saw a complementary business at a bargain price that also fit well strategically into WEICF’s portfolio. First, PSIX could help WEICF maintain access to the international market at a time when economic sanctions against China are tightening. Second, PSIX is primarily a value-added engine trader, not an engine manufacturer per se. It customizes engines from companies like Dosan, Caterpillar (CAT), General Motors (GM), Mitsubishi, and others, adding key features, components, and functions, including electrical, exhaust, and cooling systems, before selling those branded engines to its customers. It is worth noting that PSIX also manufactures its own 8.8-liter engine, which is sold to IC School Bus and other transportation original equipment manufacturers (OEMs).

Nevertheless, the PSIX acquisition was an opportunity for WEICF, one of the largest engine manufacturers in the world, to expand its presence vertically. WEICF currently holds 52% of PSIX’s outstanding shares.

Why have PSIX shares risen dramatically?

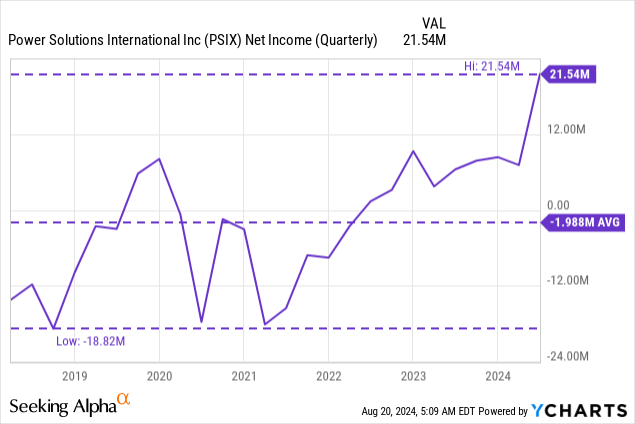

Shares rose on significantly improved margins, with net income reaching $21 million in the second quarter of 2024, the highest ever.

There are three reasons for this

- Cancellation of legal expenses after PSIX settled with the SEC regarding its past accounting errors, resulting in a $6.4 million reduction in selling and administrative expenses

- Change in product mix after PSIX abandoned its 8.8-litre engine, which proved not to be as profitable as management had hoped as it required high maintenance and service costs, which weighed on margins under warranty agreements

- Prices for steel, the main raw material for engine blocks, have fallen by 25% this year.

Of course, one cannot ignore WEICF’s turnaround efforts, including brutal cost-cutting measures and price reductions on some product lines. The cost-cutting measures are so drastic that employee turnover averages about 23% per year.

revenue

PSIX lists more than two dozen products that use its custom-engineered engines, including stationary power generators, forklifts, stump grinders, chainsaws and water pumps.

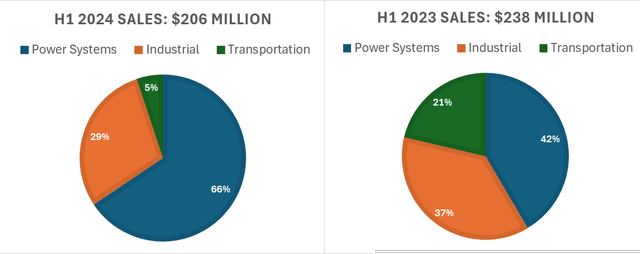

The company reports its sales primarily in three segments

- Power supply systems

- industry

- transport

For the first six months of 2024, PSIX revenues were $206 million, down 13% from the same period last year.

Author’s estimates are based on company documents

| Segments/$000 | 1st half of 2024 | 1st half of 2023 |

| Power supply systems | 135,049 USD | 99,086 USD |

| industry | 60,258 USD | 88,465 USD |

| transport | 10,519 USD | 50,783 USD |

| In total | $205,826 | $238,334 |

The transportation segment was almost completely destroyed, with revenues down 80%. PSIX is the engine supplier for IC Bus, one of the largest school bus manufacturers in the US. However, warranty costs and high maintenance fees have not made the segment as profitable as management had hoped. In addition, IC Bus is also betting on the energy transition, switching from gas, propane and diesel engines to electric drives.

The industrial segment also saw a 31% decline due to lower demand for forklift and chainsaw engines. In the forklift market, many end users, including Walmart (WMT) and Amazon (AMZN), are taking advantage of green energy credits and switching to hydrogen fuel cell modules to power their forklift fleets.

On a more positive note, PSIX sees the growing data center sector as a driver for power system sales. PSIX engines are used for air cooling, with fans attached to an engine propeller.

Looking ahead, it is difficult to identify a dominant trend driving PSIX sales. I see growth areas, such as the data center product offering. On the other hand, cyclical shifts away from fossil fuels in the material handling market and tightening regulatory environments for transportation engines, including niche markets served by PSIX, such as school buses and trucks, could permanently impact the company’s market position.

Accounting challenges and why I might be wrong

I think PSIX will deliver results in line with the broader market going forward. When you look at the two components driving margin growth behind the recent stock rally, it’s easy to see that it’s a temporary development and there’s no consistent tailwind to keep pushing the stock higher. The $6.4 million legal expense cancellation that reduced SG&A expenses by 30% last quarter is a one-time item. Improvements in warranty costs came at the expense of lower sales. Finally, steel prices fluctuate, and while they’re currently at multi-year lows, a reversal is plausible.

This is not to detract from the efforts and successes of management’s turnaround initiatives. The margin improvements are in part the result of successful rationalization of business costs.

But one cannot ignore the fact that this is a stock with an accumulated deficit of $132 million. Moreover, it is a subsidiary of a Chinese conglomerate whose interests could conflict with those of its shareholders. One can imagine a scenario in which WEICF sacrifices its subsidiary for the “greater good” of its core business.

PSIX relies on WEICF for debt financing. Most of PSIX’s borrowings are short-term loans provided by the parent company. And its second-degree liquidity is less than one (cash: $28 million versus current liabilities of $135 million). This means that if its business declines, PSIX may not be able to repay these borrowings. Its second-degree liquidity is also less than 1x.

Final thoughts

PSIX’s results in the second quarter of 2024 were quite good: gross margins increased, operating expenses decreased, and net profit reached record highs despite a decline in revenue.

However, it is important to remember that this is a stock with a cumulative deficit of $132 million. WEICF exercises significant control over PSIX as it owns the majority of the shares and also a significant portion of the debt. There is a risk that WEICF will prioritize its core business at the expense of its subsidiary PSIX as demand in several end markets shifts away from internal combustion engines.

Gross and operating margins are likely to normalize in the coming quarters. Although PSIX has made significant progress in reducing costs, some of last quarter’s results were due to temporary factors such as the reversal of legal fees and exceptionally low steel prices.

On the other hand, the ticker is worth holding considering the current valuation of 8x forward P/E. Of course, the decline in warranty costs for PSIX’s own 8.8L engine came at the expense of sales. At the same time, however, we see growth in other end markets, including data centers and potentially semiconductors, as more manufacturing projects are moved back to the US due to the Chip Act and Inflation Reduction Act, as well as expected interest rate cuts.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these securities.